Are you ready to retire? The question is actually more complicated than it first appears, because it demands consideration on two levels. First, there’s the emotional component: Are you ready to enter a new phase of life? Do you have a plan for what you would like to accomplish or do in retirement? Have you thought through both the good and bad aspects of transitioning into retirement? Second, there’s the financial component: Can you afford to retire? Will your finances support the retirement lifestyle that you want? Do you have a retirement income plan in place?

What Does Retirement Mean To You?

When you close your eyes and think about your retirement, what do you see? Over your career, you may have had a vague concept of retirement as a period of reward for a lifetime of hard work, full of possibility and potential. Now that retirement is approaching, though, you need to be much more specific about what it is that you want and expect in retirement.

Do you see yourself pursuing hobbies? Traveling? Have you considered volunteering your time, taking the opportunity to go back to school, or starting a new career or business? It’s important that you’ve given it some consideration, and have a plan. If you haven’t–for example, if you’ve thought no further than the fact that retirement simply means that you won’t have to go to work anymore–you’re not ready to retire.

Don’t Underestimate The Emotional Aspect Of Retirement

Many people define themselves by their profession. Affirmation and a sense of worth may have come, in large part, from the success that you’ve had in your career. Giving up that career can be disconcerting on a number of levels. Consider as well the fact that your job provides a certain structure to your life. You may also have work relationships that are important to you. Without something concrete to fill the void, you may find yourself scrambling to address unmet emotional needs.

While many see retirement as a new beginning, there are some for whom retirement is seen as the transition into some “final” life stage, marking the “beginning of the end.” Others, even those who have the full financial capacity to live the retirement lifestyle they desire, can’t bear the thought of not receiving a regular paycheck. For these individuals, it’s not necessarily the income that the paychecks represent, but the emotional reassurance of continuing to accumulate funds.

Finally, it’s often not simply a question of whether you are ready to retire. If you’re married, consider whether your spouse is ready for you to retire. Does he or she share your ideas of how you want to spend your retirement? Many married couples find the first few years of one or both spouse’s retirement a period of rough transition. If you haven’t discussed your plans with your spouse, you should do so; think through what the repercussions will be, positive and negative, on your roles and your relationship.

Can You Afford The Retirement You Want?

Separate from the issue of whether you’re emotionally ready to retire is the question of whether you’re financially ready. Simply, can you afford to do everything you want in retirement? Of course, the answer to this question is anything but simple. It depends on your goals in retirement (i.e., how much the lifestyle you want will cost), the amount of income you can count on, and your personal savings. It also depends on how long a retirement you want to plan for and what your assumptions are regarding future inflation and earnings.

Timing Is Everything

When it comes to transitioning into retirement, timing really is everything. The age at which you retire can have an enormous impact on your overall retirement income situation, so you’ll want to make sure you’ve considered your decision from every angle. In fact, you may find that deciding when to retire is actually the product of a series of smaller decisions and calculations.

Your Retirement: How Long Should You Plan For?

The good news is that, statistically, you’re going to live for a long time. Life expectancy has increased at a steady pace over the years, and is expected to continue increasing. In fact, in the year 2010, the census reported over 53,000 Americans over age 100. (Source: US Census Bureau, ‘Age and Sex Composition, 2010’, 2010 Census Briefs.)

That’s also the bad news, though, because that means your retirement income plan is going to have to be sufficient to provide for your needs over (potentially) a long period of time.

How long? The average 65-year-old American can expect to live for over 18.8 additional years. (Source: National Vital Statistics Reports, Volume 59, Number 4, March 2011.) As of 2015, this is even longer. Keep in mind as well that life expectancy has increased at a steady pace over the years, and is expected to continue increasing.

The bottom line is that it’s not unreasonable to plan for a retirement period that lasts for 30 years or more.

Thinking Of Retiring Early?

Retiring early can be wonderful if you’re ready both emotionally and financially. Consider the financial aspect of an early retirement with great care, though. An early retirement can dramatically change your retirement finances because it affects your income plan in two major ways.

First, you’re giving up what could be prime earning years, a period of time during which you could be adding to your retirement savings. More importantly, though, you’re increasing the number of years that your retirement savings will need to provide for your expenses. And a few years can make a tremendous difference.

There are other factors to consider as well:

- A longer retirement period means a greater potential for inflation to eat away at your purchasing power.

- You can begin receiving Social Security retirement benefits as early as age 62. However, your benefit may be as much as 20% to 30% less than if you waited until full retirement age (65 to 67, depending on the year you were born).

- If you’re covered by an employer pension plan, check to make sure it won’t be negatively affected by your early retirement. Because the greatest accrual of benefits generally occurs during your final years of employment, it’s possible that early retirement could effectively reduce the benefits you receive.

- If you plan to start using your 401(k) or traditional IRA savings before you turn 59½, you may have to pay a 10% early distribution penalty tax in addition to any regular income tax due (with some exceptions, including payments made from a 401(k) plan due to your separation from service in or after the year you turn 55, and distributions due to disability).

- You’re not eligible for Medicare until you turn 65. Unless you’ll be eligible for retiree health benefits through your employer (or have coverage through your spouse’s plan), or you take another job that offers health insurance, you’ll need to calculate the cost of paying for insurance or health care out-of-pocket, at least until you can receive Medicare coverage.

Thinking Of Postponing Retirement?

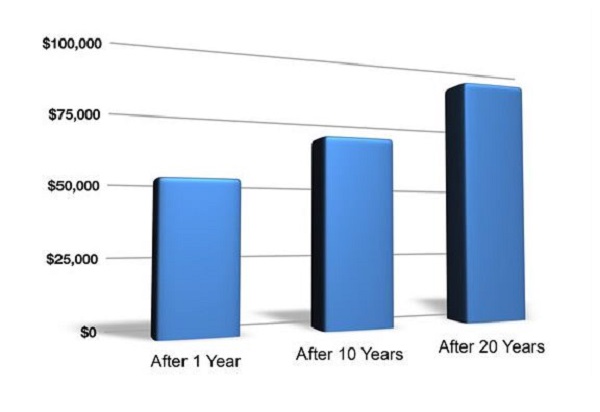

Postponing retirement lets you continue to add to your retirement savings. That’s especially advantageous if you’re saving in tax-deferred accounts, and if you’re receiving employer contributions. For example, if you retire at age 65 instead of age 55, and manage to save an additional $20,000 per year in your 401(k) at an 8% rate of return during that time, you can add an extra $312,909 to your retirement fund. (This is a hypothetical example and is not intended to reflect the actual performance of any specific investment.)

Even if you’re no longer adding to your retirement savings, delaying retirement postpones the date that you’ll need to start withdrawing from your savings. That could significantly enhance your savings’ potential to last throughout your lifetime.

And, of course, there are other factors that you should consider:

- Postponing full retirement gives you additional transition time if you need it. If you’re considering a new career or volunteer opportunities in retirement, you could lay the groundwork by taking classes or trying out your new role part-time.

- Postponing retirement may allow you to delay taking Social Security retirement benefits, potentially increasing your benefit.

- If you postpone retirement beyond age 70½, you’ll need to begin taking required minimum distributions from any traditional IRAs and employer sponsored retirement plans (other than your current employer’s retirement plan), even if you do not need the funds.

Key Decision Points

| Age | Don’t forget … | |

| Eligible to tap tax-deferred savings without early withdrawal penalty | 59.5 * | Federal income taxes will be due on pretax contributions and earnings |

| Eligible for early Social Security benefits | 62 | Taking benefits before full retirement age reduces each monthly payment |

| Eligible for Medicare | 65 | Contact Medicare three months before your 65th birthday |

| Full retirement age for Social Security | 65 to 67, depending on when you were born | After full retirement age, earned income no longer affects Social Security benefits |

* Age 55 for distributions from employer plans upon termination of employment; other exceptions apply.

How Much Annual Retirement Income Will You Need?

How much annual income will you need in retirement? If you aren’t able to answer this question, you’re not ready to make a decision about retiring. And, if it’s been more than a year since you’ve thought about it, it’s time to revisit your calculations. Your whole retirement income plan starts with your target annual income, and there are a significant number of factors to consider; start out with a poor estimate of your needs, and your plan is off-track before you’ve even begun.

General Guidelines

It’s common to discuss desired annual retirement income as a percentage f your current income. Depending on who you’re talking to, that percentage could be anywhere from 60% to 90%, or even more, of your current income. The appeal of this approach lies in its simplicity, and the fact that there’s a fairly common-sense analysis underlying it: Your current income sustains your present lifestyle, so taking that income and reducing it by a specific percentage to reflect the fact that there will be certain expenses you’ll no longer be liable for (e.g., payroll taxes) will, theoretically, allow you to sustain your current lifestyle.

The problem with this approach is that it doesn’t account for your specific situation. If you intend to travel extensively in retirement, for example, you might easily need 100% (or more) of your current income to get by. It’s fine to use a percentage of your current income as a benchmark, but it’s worth going through all of your current expenses in detail, and really thinking about how those expenses will change over time as you transition into retirement.

Factors To Consider

It all starts with your plans for retirement – the lifestyle that you envision. Do you expect to travel extensively? Take up or rediscover a hobby? Do you plan to take classes? Whatever your plan, try to assign a corresponding dollar cost. Other specific considerations include:

Housing costs: If your mortgage isn’t already paid off, will it be paid soon? Do you plan to relocate to a less (or more) expensive area? Downsize?

Work-related expenses: You’re likely to eliminate some costs associated with your current job (for example, commuting, clothing, dry cleaning, retirement savings contributions), in addition to payroll taxes.

Health care: Health-care costs can have a significant impact on your retirement finances (this can be particularly true in the early years if you retire before you’re eligible for Medicare).

Long-term care costs: The potential costs involved in an extended nursing home stay can be catastrophic.

Entertainment: It’s not uncommon to see an increase in general entertainment expenses like dining out.

Children/parents: Are you responsible financially for family members? Could that change in future years?

Gifting: Do you plan on making gifts to family members or a favorite charity? Do you want to ensure that funds are left to your heirs at your death?

Accounting For Inflation

Inflation is the risk that the purchasing power of a dollar will decline over time, due to the rising cost of goods and services. If inflation runs at its historical average of about 3%, a given sum of money will lose half its purchasing power in 23 years.

Assuming a consistent annual inflation rate of 3%, and excluding taxes and investment returns in general, if $50,000 satisfies your retirement income needs in the first year of retirement, you’ll need $51,500 of income the next year to meet the same income needs. In 10 years, you’ll need about $67,196. In other words, all other things being equal, inflation means that you’ll need more income each year just to keep pace.

How much you need to equal $50k in today’s money, given 3% inflation?  Do You Plan To Work In Retirement?

Do You Plan To Work In Retirement?

An increasing number of employees nearing retirement plan to work for at least some period of time during their retirement years. The obvious advantage of working during retirement is that you’ll be earning money and relying less on your retirement savings– leaving more to potentially grow for the future and helping your savings to last longer.

But there are also non-economic reasons for working during retirement. Many retirees work for personal fulfillment – to stay mentally and physically active, to enjoy the social benefits of working, or to try their hand at something new. The reasons are as varied as the retirees themselves.

If you’re thinking of working during a portion of your retirement, you’ll want to consider carefully how it might affect your overall retirement income. For example:

- If you continue to work, will you have access to affordable health care (more and more employers are offering this important benefit to part-time employees)?

- Will working in retirement allow you to delay receiving Social Security retirement benefits? If so, your annual benefit–when you begin receiving benefits–may be higher.

- If you’ll be receiving Social Security benefits while working, how will your work income affect the amount of Social Security benefits that received? Additional earnings can increase benefits in future years. However, for years before you reach full retirement age, $1 in benefits will generally be withheld for every $2 you earn over the annual earnings limit ($14,640 in 2012). Special rules apply in the year that you reach full retirement age.

Some employers have begun to offer phased retirement programs. These programs allow you to receive all or part of your pension benefit once you’ve reached retirement age, while you continue to work on a part-time basis for the same employer.

Retirement Income: The ‘Three-Legged Stool’

Traditionally, retirement income has been described as a “three-legged stool”, comprised of Social Security, traditional employer pension income, and individual savings and investments. With fewer and fewer individuals covered by traditional employer pensions, though, the analogy doesn’t really hold up well today.

Social Security Retirement Income

Today, 94% of U.S. workers are covered by Social Security (Source: SSA–Social Security Basic Facts, 2011). The amount of Social Security retirement benefit that you’re entitled to is based on the number of years you’ve been working and the amount you’ve earned. Your benefit is calculated using a formula that takes into account your 35 highest earning years.

According to the Social Security Administration (SSA), approximately 74% of Americans elect to receive their Social Security benefits early. ( Source: SSA Annual Statistical Supplement, 2011).

Social Security Full Retirement Age

| Birth Year | Full Retirement Age |

| 1943-1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

Source: Social Security Administration

The earliest that you can begin receiving Social Security retirement benefits is age 62. If you decide to start collecting benefits before your full retirement age (which ranges from 65 to 67, depending on the year you were born), there’s a major drawback to consider: Your monthly retirement benefit will be permanently reduced. In fact, if you begin collecting retirement benefits at age 62, each monthly benefit check will be 20% to 30% less than it would be at full retirement age. The exact amount of the reduction will depend on the year you were born. (Conversely, you can get a higher payout by delaying retirement past your full retirement age–the government increases your payout every month that you delay retirement, up to age 70.)

If you begin receiving retirement benefits at age 62, however, even though your monthly benefit is less than it would be if you waited until normal retirement age, you’ll end up receiving more benefit checks. For example, if your normal retirement age is 66, if you opt to receive Social Security retirement benefits at age 62 rather than waiting until 66, you’ll receive 48 additional monthly benefit payments.

The good news is that, for many people, Social Security will provide a monthly benefit each and every month of retirement, and the benefit will be periodically adjusted for inflation. The bad news is that, for many people, Social Security alone isn’t going to provide enough income in retirement. For example, according to the quick calculator on Social Security’s website, an individual born in 1952 who currently earns $100,000 a year can expect to receive approximately $26,500 annually at full retirement age, which in this case would be age 66. Of course, your actual benefits will depend on your work history, earnings, and retirement age. The point is that Social Security will probably make up only a portion of your total retirement income needs.

Traditional Employer Pensions

If you’re entitled to receive a traditional pension, you’re lucky; fewer Americans are covered by them every year. If you haven’t already selected a payout option, you’ll want to carefully consider your choices. And, whether or not you’ve already chosen a payout option, you’ll want to make sure you know exactly how much income your pension will provide, and whether or not it will adjust for inflation.

Your pension plan must provide you with an explanation of your options prior to retirement, including an explanation of your rights to waive the QJSA (qualified joint and survivor annuity), and the relative values of any optional forms of benefit available to you.

In a traditional pension plan (also known as a defined benefit plan), your retirement benefit is generally an annuity, payable over your lifetime, beginning at the plan’s normal retirement age (typically age 65). Many plans allow you to retire early (for example, at age 55 or earlier). However, if you choose early retirement, your pension benefit is actuarially reduced to account for the fact that payments are beginning earlier, and are payable for a longer period of time.

If you’re married, the plan generally must pay your benefit as a qualified joint and survivor annuity (QJSA). A QJSA provides a monthly payment for as long as either you or your spouse is alive. The payments under a QJSA are generally smaller than under a single-life annuity because they continue until both you and your spouse have died.

Your spouse’s QJSA survivor benefit is typically 50% of the amount you receive during your joint lives. However, depending on the terms of your employer’s plan, you may be able to elect a spousal survivor benefit of up to 100% of the amount you receive during your joint lives. Generally, the greater the survivor benefit you choose, the smaller the amount you will receive during your joint lives. If your spouse consents in writing, you can decline the QJSA and elect a single-life annuity or another option offered by the plan.

One option to consider when deciding between a single-life annuity and the QJSA is ‘pension maximization’. Under this strategy, you choose the single-life annuity, with its larger benefit, and then use the additional income to purchase life insurance with your spouse as the beneficiary, thereby providing for your spouse’s financial future.

The best option for you depends on your individual situation, including your (and your spouse’s) age, health, and other financial resources. If you’re at all unsure about your pension, including which options are available to you, talk to your employer or to a financial professional.

Personal Savings

Most people are not going to be able to rely on Social Security retirement benefits to provide for all of their needs. And traditional pensions are becoming more and more rare. That leaves the last leg of the three-legged stool, or personal savings, to carry most of the burden when it comes to your retirement income plan.

Your personal savings are funds that you’ve accumulated in tax-advantaged retirement accounts like 401(k) plans, 403(b) plans, 457(b) plans, and IRAs, as well as any investments you hold outside of tax-advantaged accounts.

Until now, when it came to personal savings, your focus was probably on accumulation–building as large a nest egg as possible. As you transition into retirement, however, that focus changes. Rather than accumulation, you’re going to need to look at your personal savings in terms of distribution and income potential. The bottom line: You want to maximize the ability of your personal savings to provide annual income during your retirement years, closing the gap between your projected annual income need and the funds you’ll be receiving from Social Security and from any pension payout.

Some of the factors you’ll need to consider, in the context of your overall plan, include:

- Your general asset allocation -The challenge is to provide, with reasonable certainty, for the annual income you will need, while balancing that need with other considerations, such as liquidity, how long you need your funds to last, your risk tolerance, and anticipated rates of return.

- Specific investments and products – Should you consider an annuity? Municipal bonds? What about a mutual fund that’s managed to provide predictable retirement income (sometimes called a “distribution” mutual fund)?

- Your withdrawal rate – How much can you afford to withdraw each year without exhausting your portfolio? You’ll need to take into account your asset allocation, projected returns, your distribution period, and whether you expect to use both principal and income, or income alone. You’ll also need to consider how much fluctuation in income you can tolerate from month to month, and year to year.

- The order in which you tap various accounts – Tax considerations can affect which accounts you should use first, and which you should defer using until later.

- Required minimum distributions (RMDs) – You’ll want to consider up front how you’ll deal with required withdrawals from tax-advantaged accounts like 401(k)s and traditional IRAs, or whether they’ll be a factor at all. After age 70½, if you withdraw less than your RMD, you’ll pay a penalty tax equal to 50% of the amount you failed to withdraw.

Other Sources Of Retirement Income

If you’ve determined that you’re not going to have sufficient annual income in retirement, consider possible additional sources of income, including:

- Working in retirement – Part-time work, regular consulting, or a full second career could all provide you with valuable income.

- Your home – If you have built up substantial home equity, you may be able to tap it as a source of retirement income. You could sell your home, then downsize or buy in a lower cost region, investing that freed-up cash to produce income or to be used as needed. Another possibility is borrowing against the value of your home (a course that should be explored with caution).

- Permanent life insurance – Although not the primary function of life insurance, an existing permanent life insurance policy that has cash value can sometimes be a potential source of retirement income. (Policy loans and withdrawals can reduce the cash value, reduce or eliminate the death benefit, and can have negative tax consequences.)

What If You Still Don’t Have Enough?

If there’s no possibility that you’re going to be able to afford the retirement you want, your options are limited:

Postpone Retirement

You’ll be able to continue to add to your retirement savings. More importantly, delaying retirement postpones the date that you’ll need to start withdrawing from your personal savings. Depending on your individual circumstances, this can make an enormous difference in your overall retirement income plan.

Reevaluate Retirement Expectations

You might consider ratcheting down your goals and expectations in retirement to a level that better aligns with your financial means. That doesn’t necessarily mean a dramatic lifestyle change–even small adjustments can make a difference.

Asset Allocation

Your asset allocation strategy in retirement will probably be different than the one you used when saving for retirement. During your accumulation years, your asset allocation decisions may have been focused primarily on long-term growth. But as you transition into retirement, your priorities for and demands on your portfolio are likely to be different. For example, when you were saving, as long as your overall portfolio was earning an acceptable average annual return, you may have been happy. However, now that you’re planning to rely on your savings to produce a regular income, the consistency of year-to-year returns and your portfolio’s volatility may assume much greater importance.

The Goal Of Asset Allocation

Balancing the need for both immediate income and long-term returns can be a challenge. Invest too conservatively, and your portfolio may not be able to grow enough to maintain your standard of living. Invest too aggressively, and you could find yourself having to withdraw money or sell securities at an inopportune time, jeopardizing future income and undercutting your long-term retirement income plan. Without proper planning, a market loss that occurs in the early years of your retirement could be devastating to your overall plan. Asset allocation alone does not guarantee a profit or ensure against a loss, but it can help you manage the level and types of risk you take with your investments based on your specific needs.

An effective asset allocation plan:

- Provides ongoing income needed to pay expenses

- Minimizes volatility to help provide both reliable current income and the ability to provide income in the future

- Maximizes the likelihood that your portfolio will last as long as you need it to

- Keeps pace with inflation in order to maintain purchasing power over time

Look Beyond Preconceived Ideas

The classic image of a retirement income portfolio is one that’s invested almost entirely in bonds, with the bond interest providing required annual income. However, retirees who put all their investments into bonds often find that doing so doesn’t adequately account for the impact of inflation over time. Consider this: If you’re earning 4% on your portfolio, but inflation is running between 3% and 4% (its historical average), your real return is only 1% at best–and that’s before subtracting any account fees, taxes, or other expenses.

Some retirees are surprised to learn that even though a bond’s interest rate may be fixed, bond prices can go up and down (though typically not as much as those of stocks). When interest rates rise, bond prices typically fall. That may not matter if you hold a bond to maturity , but if you must sell a bond before it matures, you could get less than you paid for it. Also, if you hold individual bonds or certificates of deposit, and interest rates fall before that investment matures, you may not be able to get the same interest rate if you try to reinvest that money. That could, in turn, affect your income.

That means that you may not want to turn your back on growth-oriented investments. Though past performance is no guarantee of future returns.

There’s No One Right Answer

Your financial situation is unique, which means you need an asset allocation strategy that’s tailored to you. That strategy may be a onetime allocation that gets revisited and rebalanced periodically, or it could be an asset allocation that shifts over time to correspond with your stage of retirement. The important thing is that the strategy you adopt is one that you’re comfortable with and understand.

Making Portfolio Withdrawals

When planning for retirement income, you’ll need to determine your portfolio withdrawal rate, decide which retirement accounts to tap first, and consider the impact of required minimum distributions.

Withdrawal Rates

Your retirement lifestyle will depend not only on your asset allocation and investment choices, but also on how quickly you draw down your retirement portfolio. The annual percentage that you take out of your portfolio, whether from returns or the principal itself, is known as your withdrawal rate. The higher your withdrawal rate, the more you’ll have to consider whether it is sustainable over the long term.

Take out too much too soon, and you might run out of money in your later years. Take out too little, and you might not enjoy your retirement years as much as you could. Your withdrawal rate is especially important in the early years of your retirement; how your portfolio is structured then and how much you take out can have a significant impact on how long your savings will last.

What’s the right number? It depends on your overall asset allocation, projected inflation rate and market performance, as well as countless other factors, including the timeframe that you want to plan for. For many, though, there’s a basic assumption that an appropriate withdrawal rate falls in the 4% to 5% range. In other words, you’re withdrawing just a small percentage of your investment portfolio each year. To understand why withdrawal rates generally aren’t higher, it’s essential to think about how inflation can affect your retirement income.

Consider the following example: Ignoring taxes for the sake of simplicity, if a $1 million portfolio is invested in a money market account yielding 5%, it provides $50,000 of annual income. But if annual inflation pushes prices up by 3%, more income–$51,500–would be needed the following year to preserve purchasing power. Since the account provides only $50,000 income, an additional $1,500 must be withdrawn from the principal to meet expenses. That principal reduction, in turn, reduces the portfolio’s ability to produce income the following year. As this process continues, principal reductions accelerate, ultimately resulting in a zero portfolio balance after 25 to 27 years, depending on the timing of the withdrawals.

When setting an initial withdrawal rate, it’s important to take a portfolio’s potential ups and downs into account–and the need for a relatively predictable income stream in retirement isn’t the only reason. If it becomes necessary during market downturns to sell some securities in order to continue to meet a fixed withdrawal rate, selling at an inopportune time could affect a portfolio’s ability to generate future income. Also, making your portfolio either more aggressive or more conservative will affect its lifespan. A more aggressive portfolio may produce higher returns, but might also be subject to a higher degree of loss. A more conservative portfolio might produce steadier returns at a lower rate, but could lose purchasing power to inflation.

Tapping Tax-Advantaged Accounts First Or Last?

You may have assets in accounts that are tax deferred (e.g., traditional IRAs) and tax free (e.g., Roth IRAs), as well as taxable accounts. Given a choice, which type of account should you withdraw from first?

If you don’t care about leaving an estate to beneficiaries, consider withdrawing money from taxable accounts first, then tax-deferred accounts, and lastly, any tax-free accounts. The idea is that, by using your tax-favored accounts last, and avoiding taxes as long as possible, you’ll keep more of your retirement dollars working for you on a tax-deferred basis.

If you’re concerned about leaving assets to beneficiaries, however, the analysis is a little more complicated. You’ll need to coordinate your retirement planning with your estate plan. For example, if you have appreciated or rapidly appreciating assets, it may make sense for you to withdraw those assets from your taxdeferred and tax-free accounts first. The reason? These accounts will not receive a step-up in basis at your death, as many of your other assets will.

But this may not always be the best strategy. For example, if you intend to leave your entire estate to your spouse, it may make sense to withdraw from taxable accounts first. This is because your spouse is given preferential tax treatment when it comes to your retirement plan. Your surviving spouse can roll over retirement plan funds to his or her own IRA or retirement plan, or, in some cases, may continue the plan as his or her own. The funds in the plan continue to grow tax deferred, and distributions need not begin until after your spouse reaches age 70½. The bottom line is that this decision is also a complicated one, and needs to be looked at closely.

Required Minimum Distributions (RMDs)

In practice, your choice of which assets to draw on first may, to some extent, be directed by tax rules. You can’t keep your money in tax-deferred retirement accounts forever. The law requires you to start taking distributions–called “required minimum distributions” or RMDs–from traditional IRAs by April 1 of the year following the year you turn age 70½, whether you need the money or not. For employer plans, RMDs must begin by April 1 of the year following the year you turn 70½, or, if later, the year you retire. Roth IRAs aren’t subject to the lifetime RMD rules.

RMDs are calculated by dividing your traditional IRA or retirement plan account balance by a life expectancy factor specified in IRS tables. Your account balance is usually calculated as of December 31 of the year preceding the calendar year for which the distribution is required to be made.

If you have more than one IRA, a required distribution amount is calculated separately for each IRA. These amounts are then added together to determine your total RMD for the year. You can withdraw your RMD from any one or more of your IRAs. (Similar rules apply to Section 403(b) accounts.) Your traditional IRA trustee or custodian must tell you how much you’re required to take out each year, or offer to calculate it for you. For employer retirement plans, your plan will calculate the RMD, and distribute it to you. (If you participate in more than one employer plan, your RMD will be determined separately for each plan.)

It’s very important to take RMDs into account when contemplating how you’ll withdraw money from your savings. Why? If you withdraw less than your RMD, you will pay a penalty tax equal to 50% of the amount you failed to withdraw. The good news: You can always withdraw more than your RMD amount.

Health-Care Considerations

At any age, health care is a priority. When you retire, however, you will probably focus more on health care than ever before. Staying healthy is your goal, and this can mean more visits to the doctor for preventive tests and routine checkups. There’s also a chance that your health will decline as you grow older, increasing your need for costly prescription drugs or medical treatments. That’s why having health insurance can be extremely important.

If you are 65 or older when you retire, you’re most likely eligible for certain health benefits from Medicare. But if you retire before age 65, you’ll need some way to pay for your health care until Medicare kicks in. Generous employers may offer extensive health insurance coverage to their retiring employees, but this is the exception rather than the rule. If your employer doesn’t extend health benefits to you, you might need to consider other options, such as buying a private health insurance policy or extending your employer-sponsored coverage through COBRA, if that’s a possibility.

Medicare

Most Americans automatically become entitled to Medicare when they turn 65. In fact, if you’re already receiving Social Security benefits, you won’t even have to apply – you’ll automatically be enrolled in Medicare. However, you will have to decide whether you need only Part A coverage (which is premium free for most retirees) or if you also want to purchase Part B coverage. Part A, commonly referred to as the hospital insurance portion of Medicare, can help pay for your home health care, hospice care, and inpatient hospital care. Part B helps cover other medical care such as physician care, laboratory tests, and physical therapy. You may also choose to enroll in a managed care plan or private fee-for-service plan under Medicare Part C (Medicare Advantage) if you want to pay fewer out-of-pocket health-care costs. If you don’t already have adequate prescription drug coverage, you should also consider joining a Medicare prescription drug plan offered in your area by a private company or insurer that has been approved by Medicare.

Unfortunately, Medicare won’t cover all of your health-care expenses. For some types of care, you’ll have to satisfy a deductible and make co-payments. That’s why many retirees purchase a Medigap policy.

Medigap

Unless you can afford to pay for the things that Medicare doesn’t cover, including the annual copayments and deductibles that apply to certain types of care, you may want to buy some type of Medigap policy when you sign up for Medicare Part B. There are several standard Medigap policies available. Each of these policies offers certain basic core benefits, and all but the most basic policy offer designed to cover what Medicare does not. Although not all Medigap plans are available in every state, you should be able to find a plan that best meets your needs and your budget.

When you first enroll in Medicare Part B at age 65 or older, you have a six-month Medigap open enrollment period. During that time, you have a right to buy the Medigap policy of your choice from a private insurance company, regardless of any health problems you may have.

Long-term care And Medicaid

The possibility of a prolonged stay in a nursing home weighs heavily on the minds of many older Americans and their families. That’s hardly surprising, especially considering the high cost of long-term care. Many people look into purchasing long-term care insurance (LTCI). A good LTCI policy can cover the cost of care in a nursing home, an assisted-living facility, or even your own home. But if you’re interested, don’t wait too long to buy it–you’ll generally need to be in good health. In addition, the older you are, the higher the premium you’ll pay.

Many people assume that Medicaid will pay for long-term care costs. You may be able to rely on Medicaid to pay for long-term care, but your assets and/ or income must be low enough to allow you to qualify. Additionally, Medicaid eligibility rules are numerous and complicated, and vary from state to state. Talk to an attorney or financial professional who has experience with Medicaid before you make any assumptions about the role that Medicaid will play in your overall plan.

If you found this article helpful, please SUBSCRIBE.