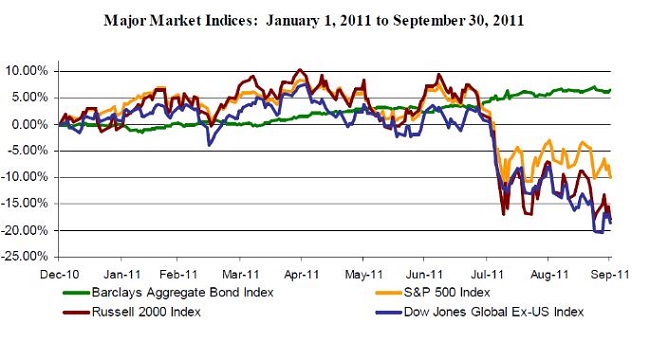

The third quarter was difficult for equity investors as stocks suffered the largest declines since the first quarter of 2009. Double digit losses occurred throughout worldwide stock markets.

What is notable is that these events did not mirror economic or corporate results. Rather, they were instigated by a lack of political decision making, with political divides leading to the first ever downgrade to our U.S. Treasuries and to a worsening debt crisis in Europe, namely in Greece.

Recent market performance suggests that the economy is too weak to support the current financial structure. While economic growth has contracted, it is still positive. And, while consumer and business sentiment have weakened, these trends have not translated into significant declines in consumption, hiring or capital spending. Bottom line, current indicators are not as strong as we would like, but they are not as dismal as the markets suggest.

In fact, the combination of rising productivity, increased capacity utilization, falling commodity prices and modestly better employment figures could lead to positive surprises in corporate earnings and market valuations. The primary caveat is that political decisions are required to enable a structural framework.

The political uncertainties that influenced third quarter losses are still present, but are hopefully reaching their pinnacles with actions required both here and in Europe before year-end. It is our opinion that the European debt crisis presents the largest risk to the global economy. Fortunately, it is also our opinion that meaningful actions should materialize within the next few weeks.

All Eyes On Europe

Extended delays in creating a solution to the European debt crisis have exacerbated problems, bringing Greece to the brink of default. While this is not an ideal scenario, it is finally forcing European hands to take action. European Union leaders are now working on efforts to support financial institutions and further backing of Greece and other EU countries is likely to follow.

Many people are wondering how the Greek crisis – which a year ago was thought to be modest in potential scope given the size of Greece relative to the world economy – is now having such a dramatic impact. We review this by addressing the many questions that clients have presented to us.

Q: Why doesn’t the EU simply pay off the Greek debt?

At first blush, this seems reasonable. The total amount of Greek debt is approximately 320 billion euros. This is far less than the amount that the EU has already infused to stabilize the debt crisis, including the latest injection of 600 billion euros. The problem is that even if Greece eliminates its outstanding debt, it does not generate enough tax revenues to support ongoing expenses. Greek state expenditures totaled approximately 70 billion euros last year as compared to tax revenues of just over 51 billion euros. As a result, funding problems would persist even if Greece could wipe its existing debt off the books.

Perhaps the largest obstacle to repaying Greek debt is the Pandora’s box it could open for the EU. Greece is not the only country with debt problems, meaning that the EU could next be faced with assuming debt obligations of Portugal, Ireland, Italy and Spain.

Q: If Greece can’t support its expenses, why don’t they reduce their spending?

Greece has dramatically reduced government spending with simultaneous tax increases to generate more revenue. The problem is that these austerity measures have caused their economy to contract. Therefore, even as taxes are going up, the economic base on which taxes are levied is declining. The economy is declining for two primary reasons. First, 40% of Greece’s economy is supported by public spending. Hence, if public spending is declining, so is the economy. Second, attachment to the highly valued euro currency is causing Greece’s goods and services to remain expensive in the global market place. If Greece had its own currency, it surely would have devalued during this crisis, helping to stimulate demand. This is in part what has helped the United States as the value of our dollar has declined.

Q: If Greece would be better off outside of the euro currency, why doesn’t Greece leave the EU?

This has been contemplated and could happen, particularly if the EU allows Greece to default. However, there are numerous complications. It took many years of planning for Greece and other countries to converge under a common euro currency. A reversal cannot happen overnight. Even if the printing presses were set in motion to reproduce drachmas (Greece’s former currency), there are further complications such as retooling ATM machines, changing financial institution programs, etc. A change in the currency would likely require an extended bank system closure which could cause a ‘run on the banks’ and problems throughout Europe.

The above comments might cause readers to question if Greece and Europe are in a ‘no-win’ situation. We do not think this is the case, but actions are required and they are required in short order. Deferral of actions have caused Europe’s debt problems to worsen and are now impacting the economies of even the strongest EU member states as well as the world economy. Confidence is quickly diminishing with numerous European debt downgrades. The best and most plausible solutions are exactly what the EU and other bodies (such as the IMF) are now exploring. These include restructuring Greece’s debt, recapitalizing European banks and possibly nationalizing Greek and other member country’s debts under a common EU structure. All eyes are on Europe to see if these or other meaningful actions ensue. We believe that positive results are likely to occur, but they will not necessarily be easy to achieve. As such, we remain cautiously optimistic of a turn in the fate of Europe.

Impact Here In the United States

The third quarter brought challenges to the US as well, namely the downgrade of our US Treasury debt. The impact of the downgrade was significant, especially with the backdrop of the European debt crisis. The global debt crisis has reduced the rate of our recovery and has added question marks about the future. However, it is important to highlight that our economy is still generating positive growth results, albeit not the robust growth that we want and need.

Recognizing that growth is more tepid than ideal, the Federal Reserve Board (Fed) commenced “Operation Twist”. This is not a James Bond or a dance move. Rather, it is a restructuring or “twisting” of our government debt obligations where the Fed will exchange $400 Billion of short-term obligations for longer-term securities. The objective is to reduce long-term interest rates in the hopes that lower rates will stimulate spending. We question the potential outcome of this latest action, particularly as rates already stood at historic lows.

At this juncture, recognizing the dramatic impact that political divides have created, we concur with US Federal Reserve Chairman Ben Bernanke’s recent comments before Congress. Bernanke stated that the Fed is prepared to take further action, but cautioned that monetary policy is not a “panacea”. Rather, he said that it is time for Congress and all economic policy makers to act together to boost the recovery.

We hope that Congressional results will finally materialize before year-end, as our political leaders face a number of deadlines when stopgap extensions to the debt ceiling and the 2012 Federal budget draw to a close. In early August, failure to agree on the debt ceiling debate led to a stopgap and creation of a Super Committee, tasked to identify deficit reductions of at least $1.2 Trillion over the next 10 years. These recommendations are due on November 23rd, with final approval by December 23rd. In late September, Congressional leaders again failed to reach agreement on the 2012 Federal budget and granted a seven week stopgap that extends through November 18th.

We expect that the year-end political process will be contentious, prompting renewed anxiety in advance of any decisions. The markets are likely to respond to such interim anxiety. However, we also expect that resolution to decisions will finally allow consumers and business leaders to move forward in planning for the future, hopefully creating positive results for the economy and the markets.

Portfolio Positioning

As stated throughout this newsletter, political indecisions here and in Europe remain the greatest immediate challenge to the investment markets. Domestically, decisions should be forced before yearend. In Europe, decisions will likely also be forced (possibly in the coming weeks) due to the state of the European debt crisis. There are no easy answers. However, if global leaders can achieve some meaningful results, the world financial structure could stabilize and resume stronger growth.

Recognizing that market volatility will likely remain elevated, we plan to continue holding modest equity exposure. Repositioning initiatives enacted throughout this year have reduced overall equity exposure and have shifted remaining equities in a more defensive posture, including dividend paying and consumer staple companies. We also reduced international exposure late last year and earlier this year, again concentrating remaining positions in a more conservative manner.

The decision to take any further action is difficult because we expect that the markets could soar if significant developments materialize. This is particularly true if we see results emerge from Europe. Virtually each time European leaders have hinted of actions, the markets have rejoiced.

SageVest Wealth Management’s current conservative bias is largely in response to the fact that we believe that capital preservation is just as important as growth to many of our clients. We encourage you to contact our office if you would like to increase equity investment exposure or to discuss your investment holdings in greater detail.

If you found this article insightful, please SUBSCRIBE.