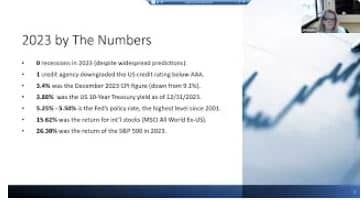

- Stocks continued upward momentum to start the year.

- Inflation has been sticky, moving slightly higher and perhaps delaying Fed rate cuts.

- Commercial real estate and issues in China present potential challenges ahead.

A Choppy but Strong Start to the Year

Stocks experienced healthy gains in the first quarter. This was primarily true for large U.S. stocks. Smaller stocks and international stocks were also up, but to a smaller degree. The movement of stock returns was choppy with many ups and downs throughout the start of the year, but the strength of gains has propelled the markets into healthy positive territory.

Sticky inflation and possible delays in Fed rate cuts hindered bond performance to start the year. Bonds experienced a modest decline as a result.

A summary of broad investment market returns as of March 31, 2024, is as follows:

Bloomberg U.S. Aggregate (U.S. bonds) -0.78%

S&P 500 Index (large U.S. stocks) 10.56%

Russell 2000 (small U.S. stocks) 5.18%

MSCI All Country World Index ex-US 4.69%

(International Stocks)

The start of the year has been optimistic and rewarding to investors. We offer a few comments relative to the quarter and looking ahead.

New All-Time Stock Highs

A number of stock markets recently set all-time highs. These include the S&P 500, Nasdaq, and Japan’s Nikkei 225 index.

The S&P 500’s returns have been heavily dominated by the “Magnificent Seven” which includes Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. These seven stocks have dominated the S&P 500’s stock returns in recent years. Apple and Tesla have stumbled this year, but the rest of the seven have continued to support U.S. market returns. Looking more broadly at the S&P 500, it’s encouraging to see that the breadth of stocks in positive territory has dramatically expanded this year showing robust overall market strength. In fact, the number of stocks trading at 52-week highs reached the highest level in the past three years.

The rally in Japan’s Nikkei 225 is a significant victory. It finally brought the index above its last record set 34 years ago in December 1989. The economy was long plagued by deflation, but price movements have thankfully improved in recent years.

The Economy

Total strength in the U.S. economy is helping to boost investment returns. The service sector, which represents the lion’s share of the economy, remains strong thanks to consumer demand. Looking at the manufacturing sector, the outlook for growth (as measured by PMI numbers) recently improved. PMI aggregates forecasts among purchasing and supply executives of manufacturing companies. A positive outlook among manufacturing executives has historically been an important economic barometer.

Looking at the labor market, employment levels have been persistently steady. This is largely good news because it keeps money flowing into consumer pockets. The one downside is it has slowed inflation declines. Strong consumer demand is a large part of what has been holding inflation in the low 3% range versus falling closer to the Fed’s target of 2%.

Outside of the United States, the global economy remains relatively healthy. There are a few exceptions including the UK, Japan, Finland, and Ireland, but the vast majority of the world’s major economies are experiencing growth.

The Fed

All eyes remain on the Fed. Inflation and related Fed actions had the most dramatic impacts on the markets in 2022 and 2023, and they will have a bearing on 2024 returns.

A few months ago, a trending decline in inflation gave the Fed confidence to announce anticipated rate cuts in 2024. Rate cuts would be widely welcomed by consumers, businesses, banks, real estate, and investment markets. However, declines in inflation have stalled. The change in the annualized CPI rate has hovered in the low to mid 3% range since October 2023. Future rate cuts remain possible in 2024, but the timing of any cuts could be delayed until the Fed feels more confident about a path toward its inflation rate target of 2%.

U.S. Budget Deficit

While a potential Fed rate cut could help to lower interest rates, it should be noted that other factors impact interest rates. One item that is front and center is the U.S. budget deficit. Historically high debt levels coupled with trillions of dollars of U.S. debt maturing over the next year will require investors to buy an estimated $10 trillion dollars of U.S. government bonds in 2024. If there isn’t enough investor demand for Treasuries, interest rates will need to move higher to attract buyers.

Real Estate

While many areas of the economy are sensitive to interest rates, a key segment that is impacted is real estate. Fortunately, the U.S. housing market has been incredibly resilient. This is largely due to lack of inventory as homeowners can’t afford to sell homes with their mortgages at ultra-low rates.

However, commercial real estate is a different animal. High interest rates and vacancy rates negatively impact valuations. A persistent work-from-home environment post-Covid has pushed vacancy rates close to 20%. SageVest doesn’t own specific real estate investments. However, a potential significant decline in commercial real estate could impact the economy and the markets, particularly given large real estate loans held on bank balance sheets.

China

On the topic of commercial real estate, the forced liquidation of China’s Evergrande Group dealt a blow to China during the first quarter. Evergrande filed for bankruptcy in 2023. In January, a Hong Kong court ordered the sale of all properties owned by the world’s most indebted developer, with over $300 billion in total liabilities.

Fortunately, the S&P 500 posted gains on the first trading day after the court order showing that Chinese events don’t necessarily ripple to the U.S markets. However, it’s important to note that problems in China’s real estate market and declines in its heavily dependent manufacturing sector present risks. China’s is the second largest economy in the world and its manufacturing sector represents a sense of global demand.

We will note that SageVest holds incredibly low exposure to China in our core investment portfolios.

U.S. Elections

Perhaps the most common question we are receiving is how the markets will react given the upcoming 2024 U.S. elections. While the future is never certain, we looked at historical S&P 500 returns in election years back to the 1970’s. The majority of election years posted positive returns. Furthermore, strong investment returns have been achieved during both Democrat and Republican administrations over this timeframe. Hence, history suggests that neither an election year nor the incumbent Presidential party means detrimental market impacts.

We continue to monitor market fundamentals on behalf of clients, implementing changes as we see appropriate without timing the markets. As always, please contact us with any questions.

SageVest Wealth Management